- Our Story

- Our Impact

-

Our Projects

Residential

Commercial

- Careers

Enquire

Enquire

Call

Call

chat

chat

Search

Search

Insight Brief: Creating and Sustaining Market for Limestone Calcined Clay Cement (LC3) in India

By Sai Sri Harsha Pallerlamudi, Tarun Garg - RMI India Foundation, Aun Abdullah - Lodha, Dr. Shashank Bishnoi - IIT-Delhi

April 01, 2025Acknowledgements: Chandler Randol – RMI, Sukanya Paciorek - RMI

Abstract:

The rapid growth and global adoption of Limestone Calcined Clay Cement (LC3) underscore its potential to transform the cement industry, particularly in the Global South, where the need for rapid infrastructure development must be met with limited clinker resources. LC3 utilises locally available raw materials that are widely available and well distributed across India, offering up to 40% reduction in carbon emissions compared to traditional Portland cement. As a sustainability-driven developer and buyer, Lodha—one of India’s leading real estate developers—is pioneering the first commercial application of LC3 in Mumbai, India. This effort, led by the Net Zero Urban Accelerator, a partnership initiative with RMI India Foundation, has provided critical insights into LC3’s market adoption.

This paper examines LC3’s potential in India’s rapidly urbanizing construction sector, particularly in the context of decarbonisation efforts and the scaling challenges of conventional supplementary cementitious materials (SCMs). It identifies key barriers to LC3 adoption, including raw material supply constraints, industry conservatism, capacity limitations, resistance from ready-mix concrete (RMC) suppliers, and regulatory hurdles. By understanding these interconnected challenges, stakeholders can design targeted interventions to accelerate LC3's market penetration, creating substantial environmental and economic value while positioning India at the forefront of cement sector decarbonisation.

Table of Contents

2. Scalability Challenges of Traditional SCMs

4. Key Findings and Learnings from field trials at Lodha

5. Challenges in LC3 Adoption in India

6. Learnings from International Markets

7. Recommendations and Call to Action: Accelerating LC3 Adoption

1. Introduction

Concrete is the most commonly used man-made material in the world. Up to 90% of this sector’s emissions arise from cement manufacturing—contributing to about 8% of anthropogenic CO2 emissions globally [1]. By 2050, global cement demand is estimated to grow by 12–23% (from 2020 levels) to 5.5 billion tonnes [2]. This growth is predominantly driven by developing nations like China and India, where rising populations, rapid urbanisation, and infrastructure development fuel demand. India ranks as the world’s second-largest cement producer, representing ~7% of global production capacity with an annual output of 0.4 billion tonnes [3].

The Global Cement and Concrete Association (GCCA) has set a target to reduce industry emission by 20% by 2030 (from 2020 levels) [4]. Most GCCA Indian member companies have already set their net-zero goals for until 2050. With clinker production accounting for approximately 60% of total cement industry CO2 emissions, reducing the clinker factor (clinker per tonne of cement) offers the highest decarbonisation potential. Industry estimates indicate that every 5% drop in clinker factor decreases CO2 emissions intensity by ~40-45kg per ton of concrete.

The average clinker factor globally is around 0.76, and for India it is around 0.71 [5][6]. Through increased share of blended cement products, the industry could potentially lower the clinker factor to just below 0.63 by 2030 [7]. Recently the Bureau of Indian Standards (BIS) in India has released an IS code (IS 18189 : 2023) for Limestone Calcined Clay Cement (LC3), a viable low-carbon alternative [8], the synergy between calcined clay and limestone allows the reduction of clinker factors to as low as 0.5 [9].

LC3 is a ternary blend, with a usual composition of clinker (50%), limestone (15%), calcined clay (30%), and gypsum (5%), capable of reducing emissions by up to 40% while maintaining performance standards comparable to OPC [9]. This paper explores LC3’s potential in India’s rapidly urbanizing construction sector, particularly in the context of decarbonisation efforts and scaling challenges for supplementary cementitious materials (SCMs). It explores key barriers to LC3 adoption, including raw material supply chain constraints, industry conservatism and capacity challenges, resistance from ready-mix concrete (RMC) suppliers, and regulatory bottlenecks. Understanding these hurdles is essential for designing targeted interventions that can accelerate LC3’s market penetration.

2. Scalability Challenges of Traditional SCMs

Reducing the clinker factor in cement production has traditionally involved incorporating SCMs such as fly ash, ground granulated blast furnace slag (GGBS), geopolymers, and composite blends. Fly-ash based Portland pozzolanic cement, typically containing 30%-35% fly ash, accounts for nearly 70% of the Indian cement market, while Portland slag cement, with 45%-60% holds around 10% [9]. Ordinary Portland cement (OPC), which consists of 90% to 95% clinker, makes up the remainder. Each of these alternatives have limitations like regional availability, codal restrictions and long-term supply security, limiting their scalability and decarbonisation potential.

2.1 Fly Ash

The Indian cement industry consumes nearly 85 MMT of fly ash (~25% of the total generated quantity)[10]. However, clinker reduction through fly ash faces critical constraints:

- Supply relies on proximity to thermal power plants, creating significant logistical challenges and regional availability and quality disparities.

- Cement standards restrict fly ash content to 35%, as higher replacement levels may negatively impact cement performance.

- Cement demand will potentially outpace fly ash supply in the long-term due to India’s Energy transition goals. The usable fly ash supply will also be reduced due to increasing generation of biomass-mixed ashes, potentially affecting their suitability for cement production.

2.2 GGBS

India produces roughly 20-30MMT of GGBS annually, as per various industry estimates [11]. Its scale does not match the scale of the current and future cement demand.

- GGBS production is inherently tied to steel manufacturing processes, making supply expansion dependent on steel industry growth rather than cement sector needs. On a global scale, GGBS availability is estimated at just 5–10% of total annual cement production, presenting a significant supply gap [12].

- GGBS is permitted in cement blends up to 50% by present standards and may not exceed 10% of cement demand in the long run.

2.3 Geopolymers and Composite Blends

Geopolymers, which replace cement with alkali-activated aluminosilicate materials, have shown promise in reducing emissions but remain confined to niche applications.

- Barriers to limited commercial adoption include complex supply chain requiring specialised raw materials, distinct production processes, and technical expertise.

- Codal permits and resistance from industry stakeholders—who prioritise proven materials with well-documented performance data—slow the adoption.

- Workforce skill gaps in safe handling of materials, such as water-glass, make the adoption at scale challenging.

2.4 LC3 as a Scalable Alternative

Currently in India, there are only three cement standards that allow the production of cements with clinker factors as low as 50%: Portland slag cement (IS455:1989), fly ash-slag based composite cement (IS16415:2015) and Portland calcined clay limestone cement (or LC3, IS18189:2023). Out of these, only LC3 offers a possibility that can be fully in control of the cement industry and does not require either fly ash or slag [12].

From a resource-efficiency stand-point, LC3 utilises locally available raw materials that are widely available and well distributed across India:

- Of India's estimated 185 billion tonnes of limestone reserves, approximately 68% is classified as cement-grade limestone (non-dolomite) [13]. However, Dolomitic or low-grade limestone (with as low as 30% CaO content) and even marble dust powder will still be suitable for use in LC3 —resources that are typically unsuitable for conventional cement manufacturing [12]. Such low purity limestones, which cannot be used in the production of clinker, are easily available in the mines being operated by the cement companies [12].

- While high-purity white China clay (with estimated reserves of 2.4 billion tonnes in India) is primarily reserved for high-value ceramic products, LC3 can be produced using lower-grade clay (with kaolinite content as low as 40%), as well as other clay minerals such as illite and montmorillonite [13]. These materials are often present as overburden in existing clay mines or remain unexploited due to aesthetic limitations such as colour, representing a significantly larger resource base than white China clay reserves [12].

This widespread availability of both low-grade limestone and clay required for LC3 production gives LC3 a distinct advantage in terms of scalability [14]. Since its production does not rely on other industrial by-products, LC3 avoids the supply chain vulnerabilities and geographic dependencies that affect traditional SCMs. Additionally, LC3's recent inclusion in India's emerging draft Carbon Credit Trading Scheme (CCTS) and offset mechanisms under construction sector further enhances its market viability and investment potential [15].The lower temperatures required for calcination of clays also increases the potential of the use of clean electricity for the process in the near future.

3. Advantages of LC3

3.1 Environmental Impact

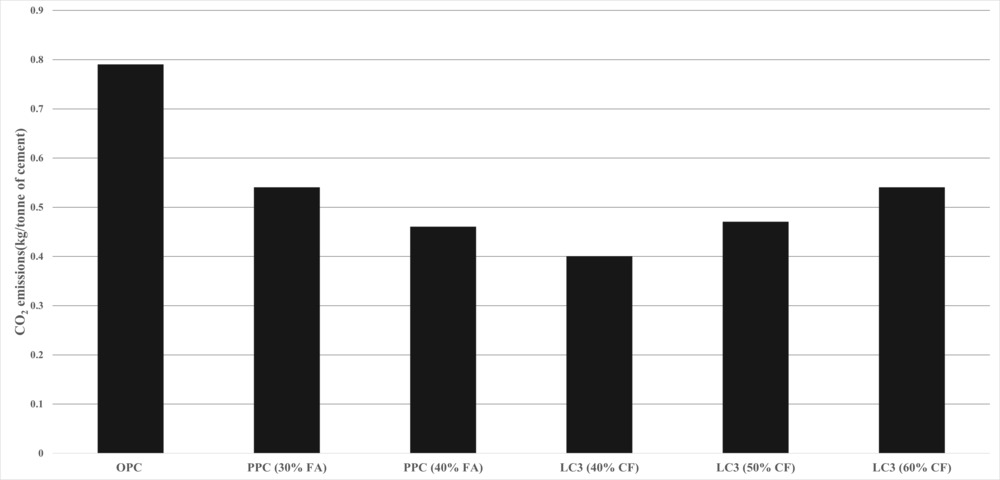

A typical LC3-50 cement blend mixture consists of 50% clinker, 30% calcined clay, 15% limestone, and 5% gypsum. As the clinker content is significantly reduced by 45%, there’s a potential to lower embodied carbon (EC) in concrete to as low as 0.06 kg CO₂e/kg and in comparison, to OPC, CO2 emissions are reduced by up to 40% compared to OPC and 11% when compared to Portland Pozzolana Cement (PPC) [9], as illustrated in Exhibit 1 below:

Exhibit 1: Estimated CO2 emissions from production of OPC, PPC and LC3 with various clinker

Source:Neha Gupta, Shashank Bishnoi, Being Sustainable yet competitive - Comparative analysis of Limestone calcined clay cement and Portland Pozzolana Cement

3.2 Performance Benefits

Research has demonstrated that LC3 exhibits comparable or superior compressive strengths comparable to OPC even when using medium-grade clay (~58% kaolinite) at a clinker factor of 0.5 [12]. Field trials at Lodha’s Palava City in Mumbai further validate its performance (see Annexure). Its enhanced resistance to chloride ingress sulphate attack makes it an excellent option for structures located in coastal areas [16][17]. Additionally, LC3's lower alkali content minimises the risk of alkali-silica reactions, improving long-term concrete performance and service life of infrastructure in aggressive environments.

3.3 Economic viability

3.3.1 CAPEX:

LC3 upgrades require retrofitting existing equipment in cement plants with clay calcination and grinding unit facilities. While a typical cement plant in India produces 1 to 3 MT of cement annually (established at a CAPEX of 100 to 300 million USD), these upgradation/retrofitting costs are relatively modest, ranging from 1 to 50 million USD [18]. Moreover, conversion from PPC to LC3 would increase production capacity due to reduced clinker consumption. Additionally, lower-grade limestone—often unsuitable for OPC—can be effectively utilised for LC3, reserving high-grade limestone for critical infrastructure applications.

3.3.2 OPEX:

Furthermore, clay calcination happens at significantly lesser temperature (700°C–800°C) compared to clinkerization temperatures (1,450°C), thus saving fuel and reducing OPEX. Therefore, in addition to its environmental savings, due to significant energy savings and use of widely available clay, LC3 also emerges as an economically viable alternative, offering up to 25% savings over OPC. The financial feasibility of LC3 depends largely on the return period of the Capex, making it commercially viable with respect to PPC in locations where the quality of fly ash is low (allowing a lower-level clinker replacement), the cost of fly ash is high, or its source is farther away than clay [18]. Carbon pricing mechanisms will further enhance LC3’s economic position.

3.3.3 Other Applications:

LC3 technology also offers versatility through a mineral additive variant, Limestone Calcined Clay (LC2), which can be used in ready-mix plants or grinding units at 15% to 45% replacement ratios of OPC, increasing concrete strength while reducing permeability—making it a cost-effective alternative to expensive additives like silica fume and metakaolin [18].

4. Key Findings and Learnings from field trials at Lodha

Lodha has set a target to reduce the embodied carbon footprint (A1-A5 LCA stages) of their buildings by 30% by 2030—from 400 to 270 KgCO2e/m2. Lodha aims to build with the smallest carbon footprint and pursues a whole-system approach across design, procurement and construction, while also exploring alternative cementitious materials. As part of these efforts, under the Net-Zero Urban Accelerator, they partnered with IIT-Delhi to initiate the first commercial use of LC3 at Lodha's pilot project site in Mumbai. IIT-Delhi is providing the necessary technical advisory for the successful completion of the project, providing compelling evidence to build confidence among developers, contractors, and industry supply chains, accelerating industry-wide acceptance. This partnership hopes to set a precedent for the commercial adoption of LC3 in the country. Concrete testing trials began in 2024, and subsequent commercial pilots are set to commence in 2025 upon availability of material, with the objective to scale it up at feasible projects at Lodha. Here are a few insights from the field trials.

4.1 Concrete Workability and Flowability

| Trial Stage | Observations | Results |

|---|---|---|

| Initial Trial | Lower concrete workability when traditional admixtures are used. There is a need for specialised admixtures. | Initial Trial Lower concrete workability when traditional admixtures are used. There is a need for specialised admixtures. Flow measurements: Initial: 520 mm (Target: 620-610 mm) After 1 hour: 470 mm (Target: 600-570 mm) After 2 hours: 450 mm (Target: 550-530 mm) After 3 hours: 430 mm (Target: 520-480 mm) |

| Process Improvement | Modified admixture addition method and specialised admixtures required. | Improved workability achieved by adding admixture to water before mixing with concrete, though flowability remained insufficient. |

| Chemical Optimisation | Admixture modifications required | Chemical Optimisation Admixture modifications required Adding 15 ml of acid to the admixture improved flowability while also reducing the total admixture volume by 10%. |

4.1.1 Key Findings:

LC3 concrete mixes can be adjusted to meet required slump and slump loss specifications. Production of flowable LC3 concrete requires optimised admixture formulations and mixing sequences. Selecting the right retarder will enhance performance.

4.2 Concrete Strength Development

| Evaluating strength gain beyond 28 days: | Evaluating strength gain beyond 28 days: | Target Strength for M30 Concrete: 38.25 MPa |

|---|---|---|

| Age | Strength (MPa) | Percentage of Target (38.25 MPa) |

| 3-day | 14.08 | 36.8% |

| 7-day | 24.5 | 64.1% |

| 28-day | 36.0 | 94.2% |

4.1.2 Key Findings:

No significant strength increase observed between 28 to 90 days under standard curing conditions. The final strength was lower-than-expected due to the use of citric-acid as a retarder. However, strength-gain is possible with adequate availability of water and the use of more suitable admixtures. LC3 is seen to demonstrate a better performance with higher-grade concretes, however, the need for better admixtures is even more important.

4.3 Material Properties

| Property | Observation | Technical Assessment |

|---|---|---|

| Fineness | Higher Blaine fineness value observed. | Fineness Higher Blaine fineness value observed. High Blaine fineness may not directly correlate to increased shrinkage cracks. Many factors influence the cracking risk at the same time. Blaine is not an appropriate test for LC3 cement due to difference in particle morphology. Many field trials in pavement construction using LC3 carried out in other pilots, have shown no signs of increased cracking. |

| Normal Consistency (NC) | Higher NC value observed. | Initial concern about higher NC value resulting in higher water demand, potentially reducing strength were addressed in subsequent trials. Solutions for managing higher water demand successfully tested and implemented. More suitable admixtures are required for continued commercial usage. |

4.4 Way forward

The field trials demonstrated that with proper mix design adjustments and admixture optimisation, LC3 can achieve the required performance specifications for construction applications. While some initial challenges with workability and water demand were encountered, these were successfully addressed through targeted interventions. These results provide a strong technical foundation for the upcoming commercial implementation at Lodha's Mumbai project site. Discussions are underway with broader supply chain to procure 1000 tonnes of LC3 for further tests and pilots and with RMC and admixture suppliers to develop workable formulations, further validating LC3's viability for mainstream construction applications in India.

5. Challenges in LC3 Adoption in India

India stands at a critical inflection point in cement decarbonisation. While LC3 offers compelling environmental and performance advantages, its widespread adoption faces barriers across the entire value chain—from raw material sourcing to construction site implementation. Our experience implementing the first commercial application of LC3 in Mumbai, India, provides key insights into the challenges of scaling LC3. We have learnt that unlocking LC3’s market potential requires strategic interventions across five key dimensions: Capacity, Chemistry, Confidence, Compliance, and Capital.

5.1 Capacity: Scaling Supply Chain and Production Infrastructure

From Infrastructure Gaps to Industry Innovation

a) While global momentum is growing—with nine LC3 plants already operational worldwide, and more in planning stages- India doesn’t have its first commercial-scale LC³ production yet, despite emerging demand signals from buyers.

- Engagement with various cement manufacturers reveals that although some plants have made ad hoc arrangements to calcine clays at a large scale, there is hesitation to invest in production without assured demand, creating a classic chicken-and-egg dilemma between supply and demand.

- Example: Lodha, India’s leading real-estate developer has committed to using LC3 but continues to struggle to secure supply beyond small-scale trials with IIT Delhi [19][20].

b) Cement plants typically operate year-round, making process upgrades challenging due to operational pressures, potential production disruptions and require significant effort and stakeholder persuasion to convert existing facilities or set-up new plants.

b) Cement plants typically operate year-round, making process upgrades challenging due to operational pressures, potential production disruptions and require significant effort and stakeholder persuasion to convert existing facilities or set-up new plants.

5.2 Chemistry: Optimizing Mix Design and Admixture Compatibility

From Product Stabilisation to Performance Assurance

a) LC3 Concrete trial mixes currently require longer development cycles due to variability in cement quality from the relatively small-sized pilot-scale productions that have been carried out this far.

- Regional variations in aggregate quality and clay composition lead to performance uncertainties until stabilised and need more localised experimentation.

- Achieving kiln equilibrium for consistent high-quality production is an iterative, time-intensive process, further delaying material availability.

- Development of compatible concrete admixtures remains an open area necessitating mix design adjustments for consistent LC3 performance.

b) Difference in setting times and workability raise concerns about operational efficiency for the developers.

5.3 Confidence: Building Industry Trust and Market Momentum

From Skills Gaps to Workforce Readiness

a) The construction sector is inherently risk-averse and slow to adopt new materials, requiring large-scale field data from pilot projects before broader adoption by developers and government organisations.

b) Limited familiarity and training around handling LC3-based concrete mix designs discourages project and construction teams from adoption.

5.4 Compliance: Creating an Enabling Environment

From Fragmented Efforts to Integrated Policy Action

a) While policy frameworks are evolving to support low-carbon cement alternatives, and the recent BIS code for LC3 and its inclusion in carbon offset mechanisms mark progress, but regulatory approvals for plant upgrades are slow, hindering commercial production.

b) Despite BIS recognition, building codes (NBC, ECBC, ENS), schedules of rates and municipal by-laws lack uniform guidance on low-carbon cement. Current cement regulations are largely prescriptive, favoring traditional materials. lack of performance-based standards—for evaluating materials on strength, durability, and emissions—also restrict LC3 to compete on equal footing.

5.5 Capital: Aligning Investments and Incentives

From High Upfront Costs to Scalable Market Growth

a) While ultimately more economical in the long-term, LC3 production ends up being more expensive in the early stages of development, deterring scale-up.

b) Cement manufacturers require significant investments to retrofit plants for LC3 production, but such capital investments are not forthcoming in the absence of established market demand. Additional infrastructure costs further discourage ready-mix suppliers from early adoption, who are also hesitant to invest in admixture reformulation without assured buyers.

c) Though large buyers, such as Lodha, while may source LC3 from distant plants for a pilot, unavailability of proximal production adds to transportation costs, erode economic and environmental benefits, and acts as a deterrent even for trials.

6. Learnings from International Markets

The global cement industry offers valuable lessons for accelerating the adoption of LC3, particularly in overcoming economic and regulatory barriers.

One of the most significant challenges for LC3 adoption, especially in the U.S., is the CAPEX required for retrofitting kilns and supporting storage infrastructure. This financial barrier has limited early investment, though targeted policy support has played a role in enabling initial projects. For example, in the U.S., Inflation Reduction Act (IRA) funding helped cement companies begin deploying clay calcination, highlighting the importance of financial incentives in market transformation [21].

China is also advancing LC3 production, with its first pilot production line in Nanjing demonstrating technical feasibility at scale. However, economic hurdles remain. Traditional SCMs like fly ash and blast furnace slag are still more cost-competitive, limiting LC3 adoption. Additionally, variability in clays presents supply chain challenges that must be addressed for broader market deployment.

Despite the upfront investment required, reduced operational expenses (OPEX) have been a key driver for LC3 deployment, particularly in regions with high clinker costs or heavy reliance on clinker imports. RMI’s plant-level analysis, which spans facilities in Africa, Latin America, the U.S., and the EU, indicates that producing LC3 can reduce OPEX by 12–33% per ton compared to (OPC) [22]. This advantage stems from LC3’s lower clinker content, the reduced energy consumption in the calcination process and possibility to blend larger quantities of uncalcined limestone, making it a financially compelling alternative.

Another emerging pathway for broader LC3 adoption is the potential role of modular kilns. Unlike traditional large-scale cement kilns, modular kilns could enable a wider range of stakeholders—including entities beyond traditional cement producers—to participate in calcined clay production [22]. This decentralised approach could help scale LC3 production more rapidly and distribute cost burdens across different players in the value chain.

Despite these economic and technological advantages, global standards and codes remain a key barrier to widespread LC3 adoption. In both the U.S. and the EU, regulatory hurdles and the slow pace of code updates have constrained market entry [22]. In contrast, India has taken a proactive approach by establishing IS 18189:2023, a comprehensive standard that provides clear guidelines for the production, testing, and use of LC3-based concrete [19]. By setting a regulatory precedent, India’s approach may serve as a model for other markets seeking to facilitate LC3 deployment.

These international experiences illustrate both the opportunities and challenges for scaling LC3. Policy incentives, cost reductions, and technological innovations such as modular kilns can help drive adoption, but overcoming regulatory barriers remains critical. By learning from global markets, stakeholders can identify strategies to accelerate LC3 implementation and achieve meaningful emissions reductions in the cement industry.

7. Recommendations and Call to Action: Accelerating LC3 Adoption

A key barrier precluding market transformation in the concrete industry is a lack of alignment amongst key value chain stakeholders. To address this gap, it is critical to work with key concrete industry stakeholders to identify common actionable paths forward for creating and sustaining level playing markets for LC3 and other low carbon concrete (with clinker factors below 0.5). The Clean Concrete Pledge Initiative, offers a framework for collective action to deliver clean concrete at scale, driving down climate pollution and creating economic opportunity. The pledges may be organised into following key categories:

7.1 Buyers Pledge: By leading consumers like major concrete buying state agencies and corporates, pledging a certain share of their annual demand for low carbon concrete. These consumers can also enable joint demonstration projects to build confidence in the low carbon concrete solutions.

7.2 Suppliers Pledge: By cement and/or Ready-Mixed Concrete Companies committing to meet the generated demand.

7.3 These pledges can be supported by policy efforts like:

- National and sub-national agencies integrating low carbon concrete in the existing building codes (ECBC, ENS), Building materials compendium, General Development Control Regulation (GDCR) and Byelaws

- Transitioning to performance-based standards from prescriptive based standards

- Fast-tracking approvals for plants and low carbon concrete

- Providing tax incentives for low-carbon cement and concrete

Market Accelerators and the Financing ecosystem can further facilitate an accelerated adoption of low carbon concrete by helping industry overcome the first cost barriers through innovative financing mechanisms and development of new business models for this transition.

8. References

[1] RMI, “https://rmi.org/unlocking-global-cement-and-concrete-decarbonisation/.”

[2] International Energy Agency, “Technology Roadmap - Low-Carbon Transition in the Cement Industry,” 2018. [Online]. Available: www.wbcsdcement.org.

[3] V. Malik, M. Sharma, and A.I. Raza, “Cementing growth: Opportunities and Challenges in India’s cementing sector,” 2024.

[4] “2020 to 2030 – The decade to make it happen.” Accessed: Mar. 20, 2025. [Online]. Available: https://gccassociation.org/concretefuture/2020-2030-the-decade-to-make-it-happen/

[5] Wbcsd, “Low Carbon Technology Roadmap for the Indian Cement Sector: Status Review 2018,” 2018.

[6] “GNR 2.0 – GCCA in Numbers.” Accessed: Mar. 20, 2025. [Online]. Available: https://gccassociation.org/sustainability-innovation/gnr-gcca-in-numbers/

[7] R. Ravi and K. Lahoti, “A concrete road for net-zero emissions,” 2021.

[8] BIS, “IS 18189: 2023.” Accessed: Mar. 20, 2025. [Online]. Available: https://www.services.bis.gov.in/php/BIS_2.0/dgdashboard/Published_Standards_new/standards?commttid=MTkw&commttname=Q0VEIDI%3D&aspect=&doe=&from=2022-07-03&to=2023-07-03

[9] N. Gupta and S. Bishnoi, “Being Sustainable yet competitive-Comparative analysis of Limestone calcined clay cement and Portland Pozzolana Cement.”

[10] GOI, MoP, MoEF, CEA, and CPCB, “Ash Availability & Utilization Portal.” Accessed: Mar. 25, 2025. [Online]. Available: https://mapp.ntpc.co.in/masha/#/utilisation

[11] Indian Bureau of Mines, “Indian Minerals Yearbook,” 2022.

[12] S.h Krishnan et al., “Industrial production of limestone calcined clay cement: experience and insights,” Green Mater, 2019.

[13] Ministry of Mines, “Limestone and other Calcareous materials - Indian Minerals Yearbook 2015 (Part-III: Mineral Reviews),” 2017.

[14] Y. Cancio Díaz et al., “Limestone calcined clay cement as a low-carbon solution to meet expanding cement demand in emerging economies,” Dev Eng, vol. 2, pp. 82–91, 2017, doi: 10.1016/j.deveng.2017.06.001.

[15] BEE, “BEE Office Memorandum: Approved Sectors in Offset Mechanism under CCTS by Central Government,” 2024. [Online]. Available: www.beeindia.govin

[16] Y. Dhandapani, T. Sakthivel, M. Santhanam, R. Gettu, and R. G. Pillai, “Mechanical properties and durability performance of concretes with Limestone Calcined Clay Cement (LC3),” Cem Concr Res, 2018.

[17] C. Yu, Z. Li, and J. Liu, “Degradation of limestone calcined clay cement (LC3) mortars under sulfate attack,” Low-carbon Materials and Green Construction, vol. 1, no. 1, Feb. 2023, doi: 10.1007/s44242-022-00003-1.

[18] S. Joseph, S. Bishnoi, and S. Maity, “An economic analysis of the production of limestone calcined clay cement in India,” 2016.

[19] R. L. Swathi Shantha Raju, “Unleashing the Potential of Limestone Calcined Clay Cement (LC3).” Accessed: Mar. 20, 2025. [Online]. Available: https://rmi.org/unleashing-the-potential-of-limestone-calcined-clay-cement/

[20] Lodha, “Catalysing India’s decarbonisation: market-based solutions to accelerate sustainable growth in built environment.” Accessed: Mar. 20, 2025. [Online]. Available: https://www.lodhagroup.com/blogs/sustainability/catalysing-Indias-decarbonisation-market-based-solutions-to-accelerate-sustainable-growth-in-built-environment

[21] Jeff St. John, “The ‘clean cement’ projects getting $1.5B in Biden admin funds,” 2024. Accessed: Mar. 25, 2025. [Online]. Available: https://www.canarymedia.com/articles/clean-industry/the-clean-cement-projects-getting-1-5b-in-biden-admin-funds

[22] C. Randol, B. Skinner, S.R. Swathi, and S. James, “The Business Case for LC3 A Global Solution for Low-Carbon, Low-Cost Cement.” [Online]. Available: https://rmi.org/insight/the-business-case-for-lc3.